A firm budget

Enoch Godongwana has done a great job. Now other ministers must follow.

Published last week on Our Long Walk: Imagining progress | OLW podcast with Bill Easterly | My talk on research quality | Coming up: Join me at Stellenbosch University on Friday, 13 March as I interview Tyler Cowen live! | Thank you for subscribing. Please consider a paid subscription.

In February 2026, South Africa’s new Minister of Finance, Enoch Godongwana, tabled his fifth national budget. The headlines, as always, focused on what it means for ordinary South Africans: a slight increase in the VAT rate, adjustments to personal income tax brackets, a sin tax tweak here, a fuel levy there. What attracted less attention is something arguably more consequential. This budget contains the most firm-focused set of tax proposals in at least a decade.

Here’s why it matters. South Africa desperately needs growth. Growth, by definition, is producing more with the same number of inputs. It is firms, not households, that produce. For long our focus has been on the household: on poverty reduction, redistribution, social grants, free basic services. That is important – it is indeed the government’s responsibility to fulfil the Constitution, which gives everyone the right to food, water and shelter – but you cannot do those important things without expanding the pool of funds allowing you to do so.

And firms do more than just produce. They create jobs – the most serious social issue in South Africa. With more than a third of working-age adults unemployed on the broad definition, and youth unemployment closer to 60%, the country faces what the National Planning Commission once called a ‘ticking time bomb’. We should do all in our power to help firms establish, grow and flourish.

What does the research tell us about how that happens? A large and growing economics literature has studied firm dynamics in developing countries. Verhoogen (2023), in a comprehensive review, identifies three categories of drivers that help firms upgrade: conditions on the output side (access to richer markets and demanding buyers), conditions on the input side (affordable credit, quality intermediate goods, skilled labour), and what he calls ‘know-how’ – the managerial and technical capabilities that must often be built from within.1 The lesson is that firms in developing countries are not failing because their entrepreneurs are lazy. They are optimising under constraints: thin markets, poor infrastructure, scarce information, and regulatory friction.

A recent study by Visagie, Turok and Nell (2026), using South African tax data, provides striking evidence of this.2 Business churn in South Africa is actually comparable to OECD levels: about 11% of firms are new entrants each year. The problem is not a lack of births; in other words, we don’t have a lack of entrepreneurial ideas. It is that creation mirrors destruction. For every firm that enters, almost as many exit. The net growth rate is slim, and structural transformation – the shift of resources from less to more productive sectors – has stalled. Put differently, the engine is turning over, but the car is not moving forward.

One reason is that small firms really struggle. Kreuser and Newman (2018), using the same administrative tax data, confirm that there is enormous heterogeneity in productivity across South African manufacturing firms.3 Larger firms are significantly more productive. Firms that trade internationally and invest in research and development show a clear productivity premium. Yet many firms remain small, unproductive and unable to scale – trapped below the threshold at which they might begin to benefit from what Garetto et al. document as the technology transfers and know-how spillovers that come with foreign direct investment. In their comprehensive review, Garetto and colleagues show that multinational enterprises raise real incomes in host countries primarily through technology transfer and the sharing of management know-how. But these gains depend on local conditions: the quality of infrastructure, the depth of the labour market, the predictability of the regulatory environment. In short, the enabling environment matters.

Which brings us back to the 2026 Budget. Consider what has changed.

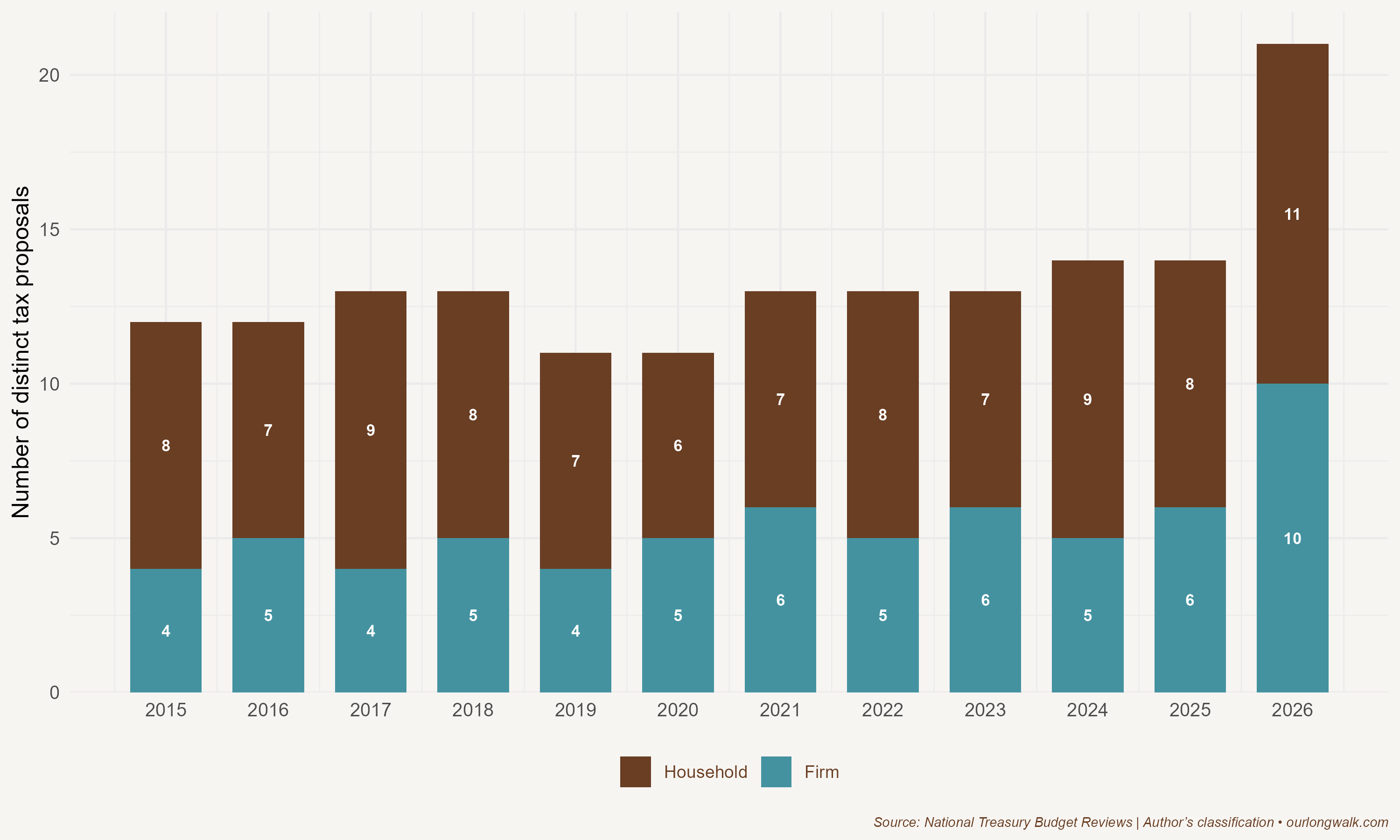

The stacked bars above count the number of distinct tax proposals directed at firms versus households in each budget since 2015. The pattern is clear: household measures have consistently outnumbered firm measures. In 2026, for the first time, the number of firm-focused proposals – 10 – nearly matches the household count. The budget introduces a reformed special economic zone regime, raises the employment tax incentive, simplifies the turnover tax for small businesses, adjusts provisional tax thresholds, implements global minimum tax rules, and overhauls the VAT registration threshold.

That last measure deserves closer inspection.

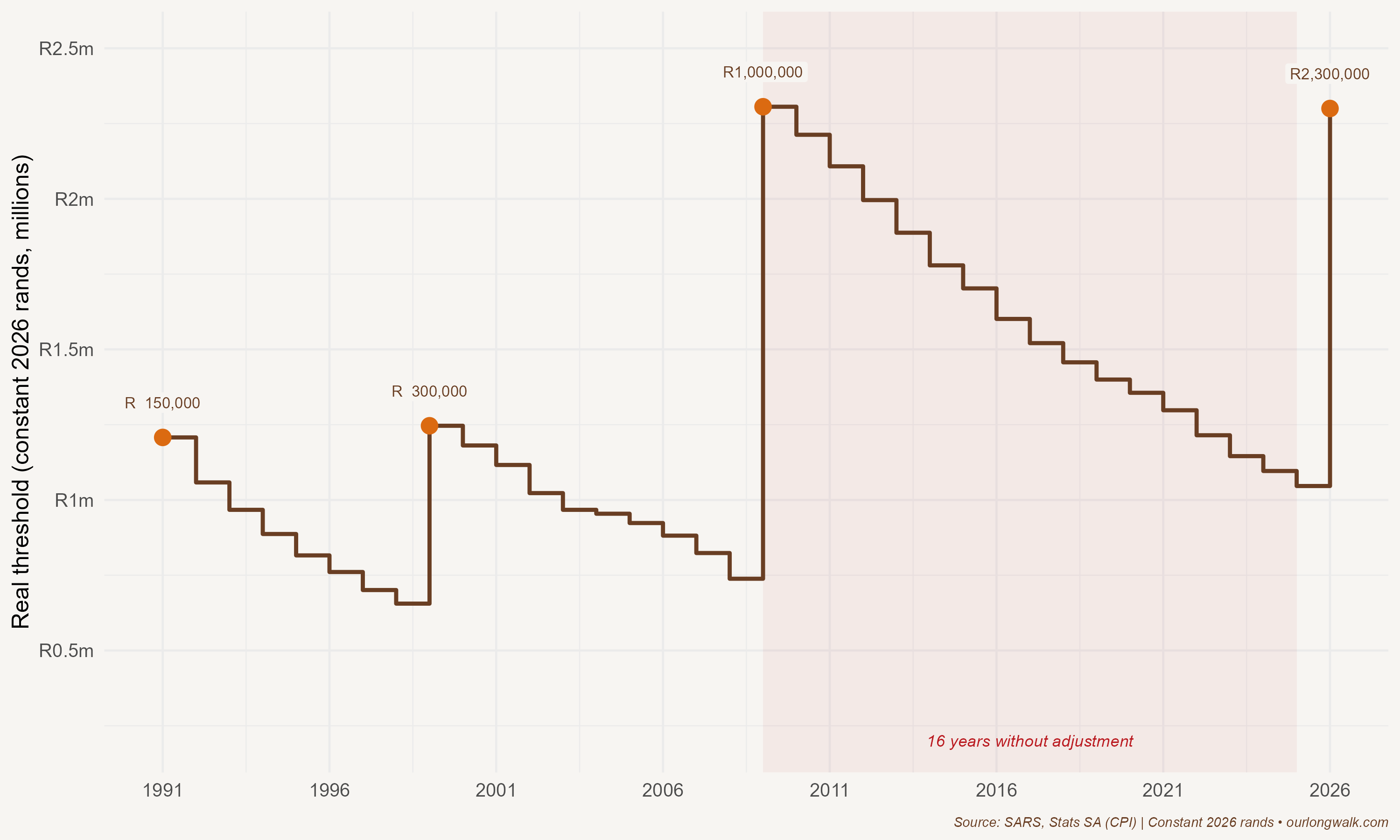

The VAT compulsory registration threshold – the turnover level above which a business must register for VAT – was set at R1 million in 2009. It stayed there for sixteen years. In real terms, as the figure above shows, this meant the threshold eroded steadily, dragging ever-smaller businesses into the compliance net. A business turning over R1 million in 2025 was, in purchasing-power terms, equivalent to one turning over roughly R600 000 in 2009. The 2026 budget raises the threshold to R2.3 million, the first adjustment in a generation.

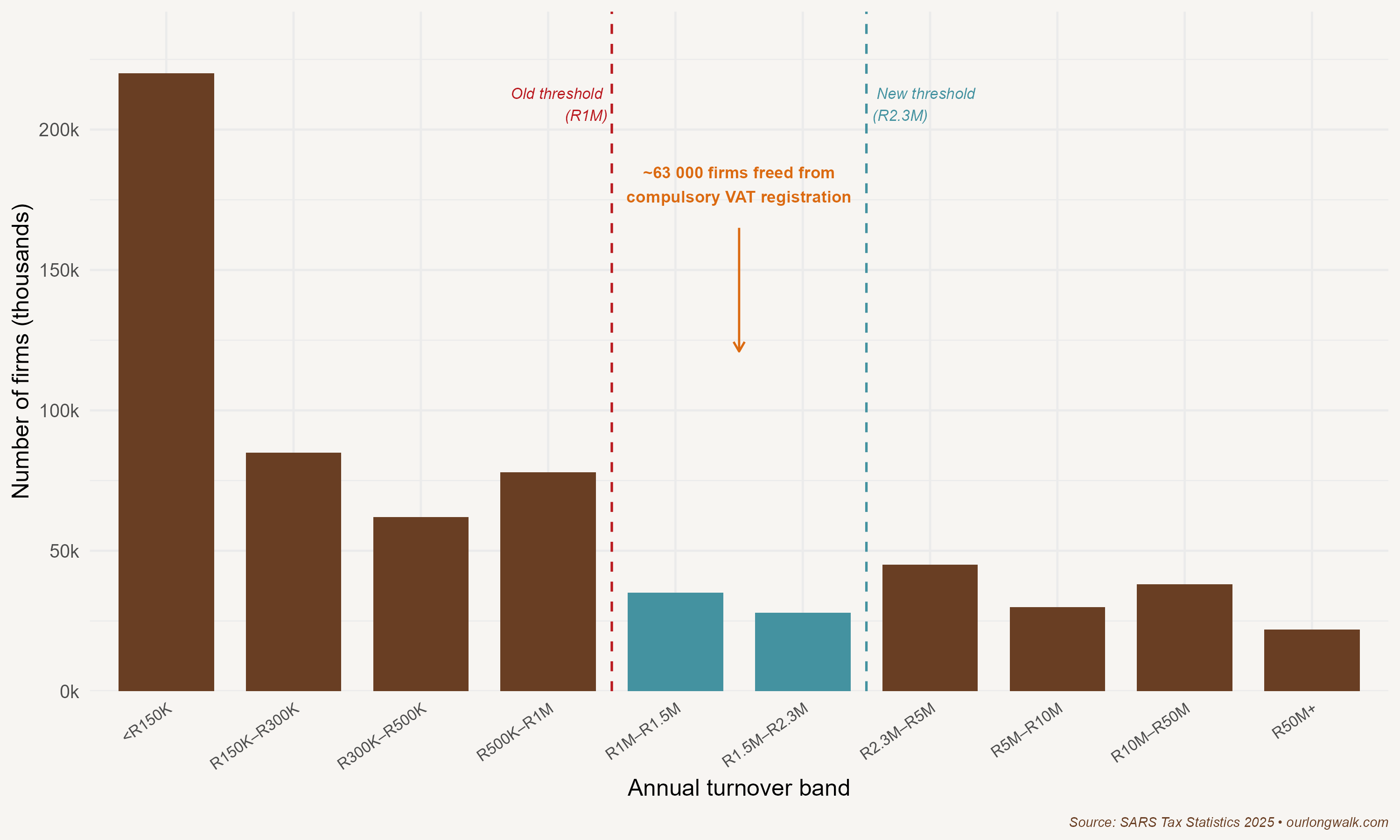

The impact is not trivial. Roughly 63 000 firms fall in the turnover band between R1 million and R2.3 million – the ‘missing middle’ of the small business distribution. These firms are now freed from compulsory VAT registration, along with the bookkeeping burden and cash-flow cost it entails. For a small manufacturer or a township retailer, this is not an abstraction. It is the difference between spending Wednesday doing paperwork and spending Wednesday serving customers.

How does the broader tax environment compare?

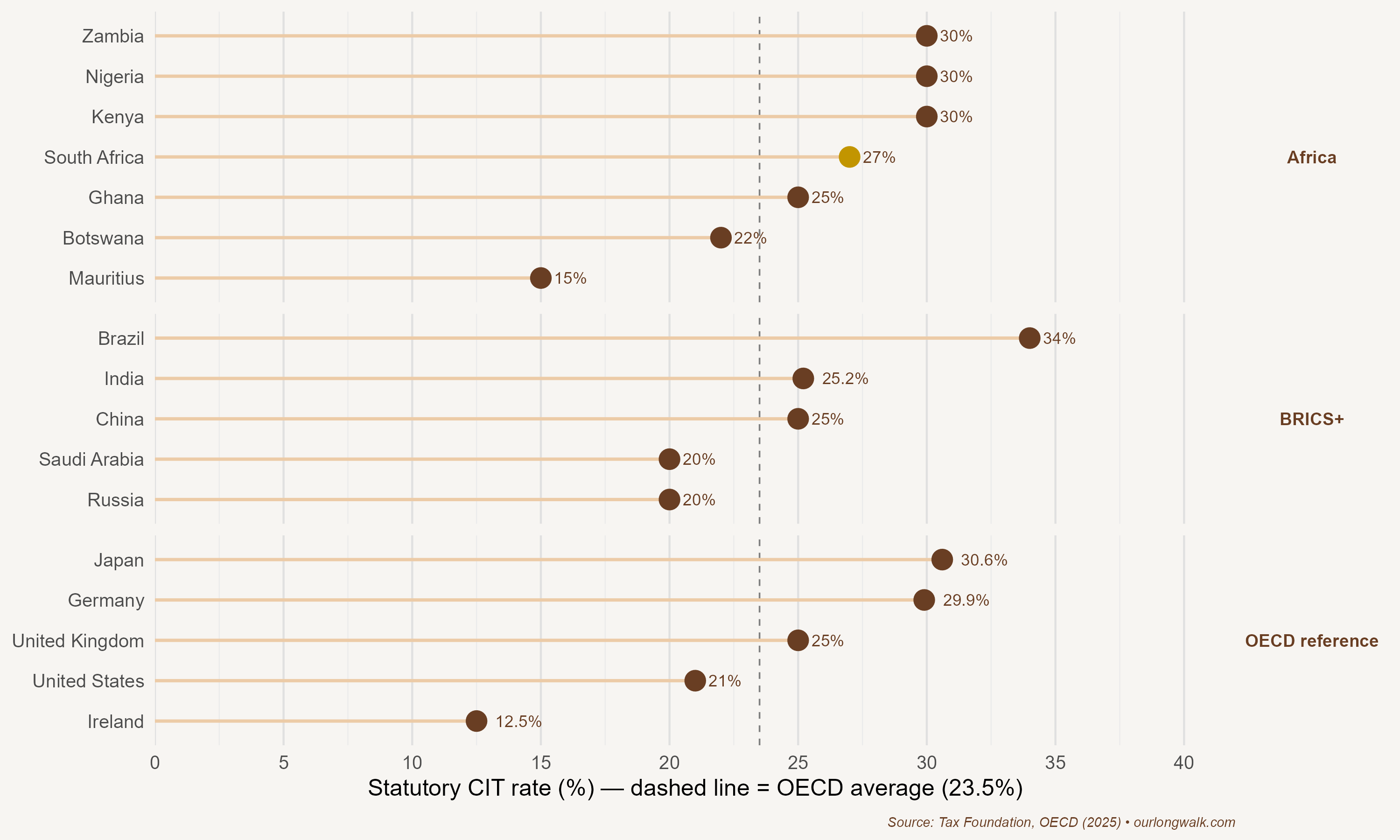

South Africa’s corporate income tax rate of 27%, reduced from 28% in 2022, sits comfortably below many African peers (Nigeria, Kenya and Zambia at 30%) and well below Brazil’s effective rate of 34%. It is marginally above the OECD average of 23.5%. The budget did not change the CIT rate, but the introduction of Pillar Two global minimum tax rules – ensuring that large multinationals pay at least 15% wherever they operate – signals that South Africa is aligning with international norms. For multinational firms considering where to locate, regulatory predictability matters as much as the rate itself.

And the government is putting money where its mouth is, at least on paper.

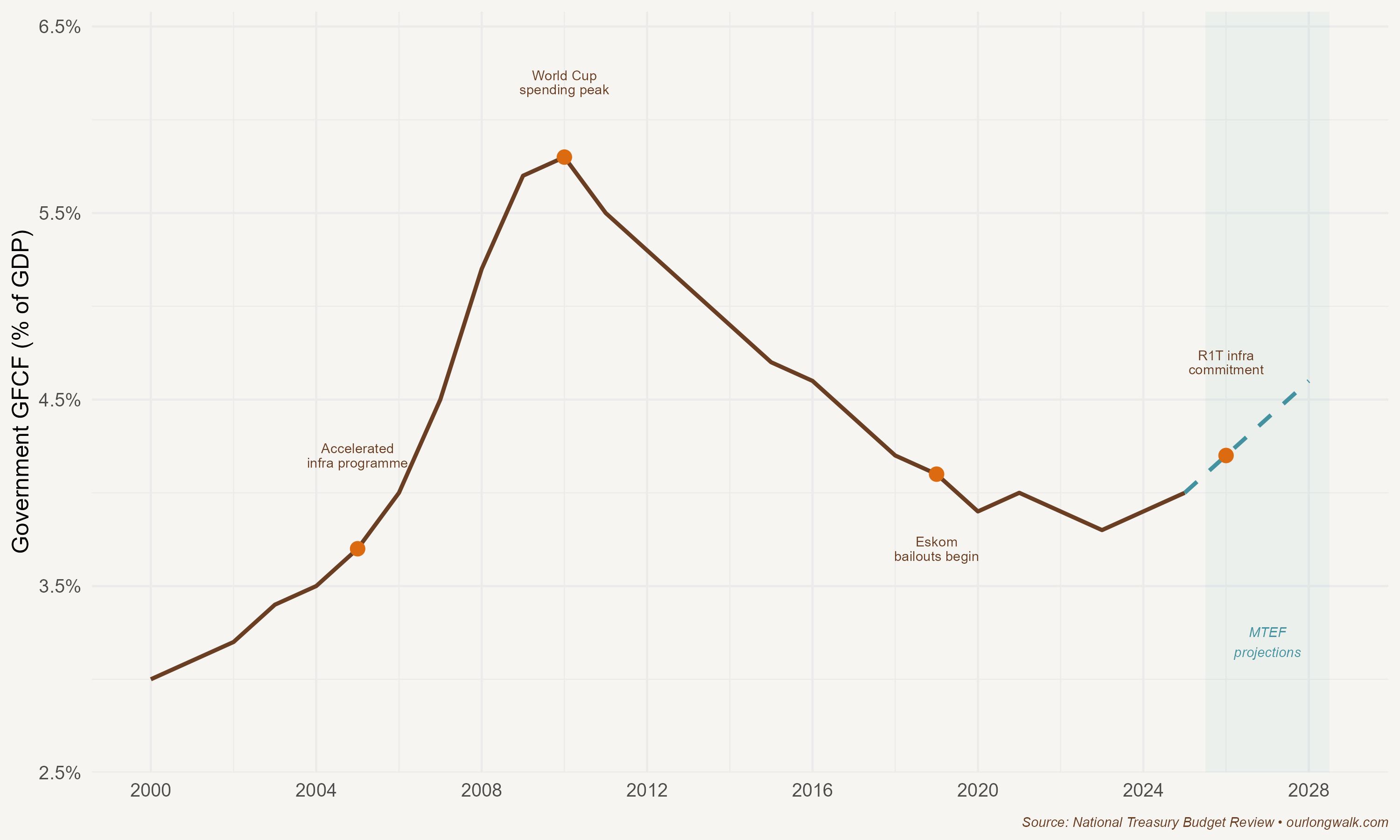

Government infrastructure investment, which peaked at nearly 6% of GDP during the World Cup build-up, has been in decline for over a decade. The Eskom crisis, Transnet dysfunction and municipal collapse all took their toll. The 2026 budget commits to reversing this trend, with gross fixed capital formation projected to rise to 4.6% of GDP by 2028/29. Whether these projections materialise is another question. But the direction – and the R1 trillion infrastructure commitment announced in the budget speech – is encouraging.

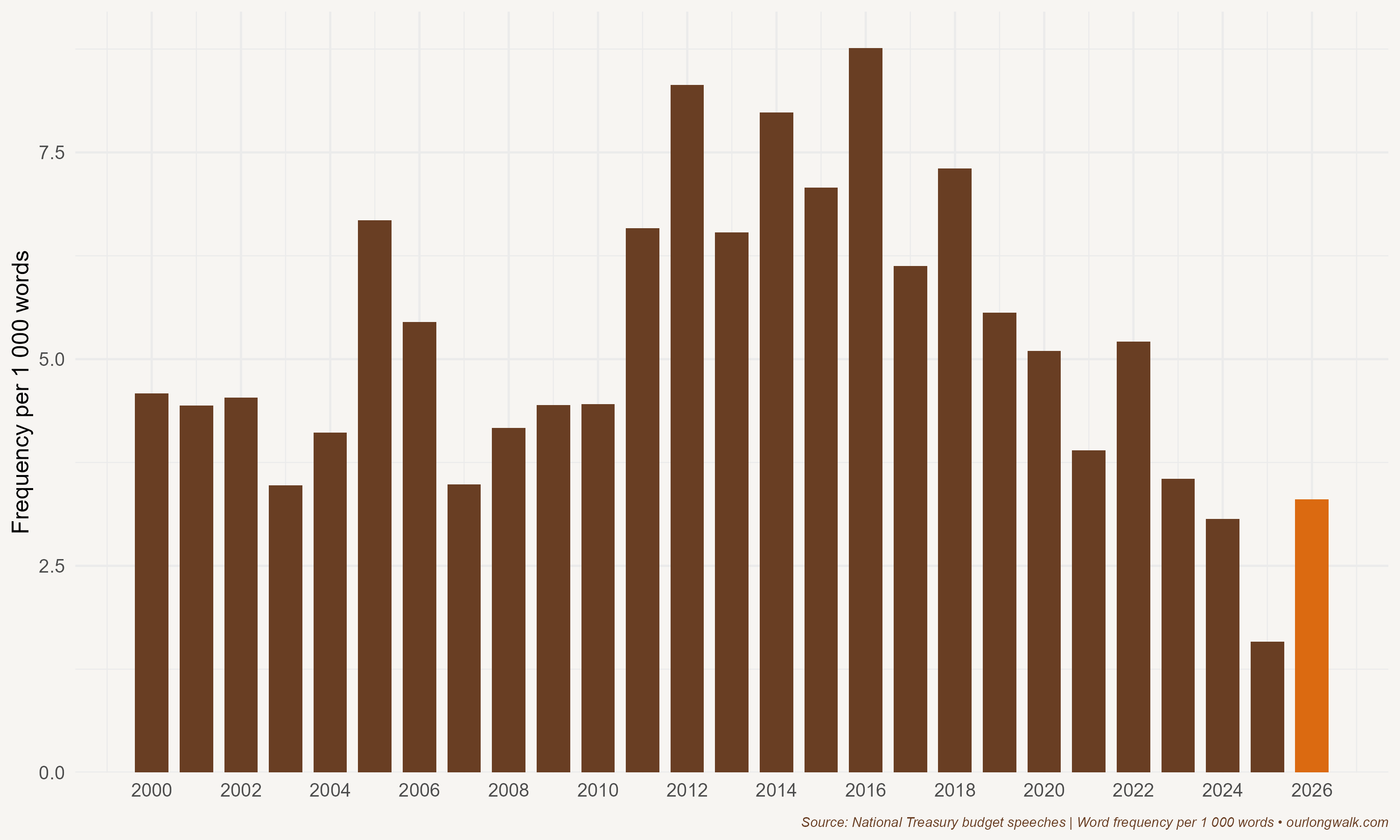

Interestingly, the budget speech itself does not use firm-related language as frequently as speeches from the 2012–2017 period. The 2026 speech scores around 3 firm-related words per 1 000, compared with peaks of 8 or more a decade ago. One reading of this is encouraging: the government is spending less time talking about business and more time actually doing something about it. Words like ‘enterprise’ and ‘private sector’ were easy rhetorical fillers in the Zuma era. What the 2026 budget offers instead is specificity – concrete changes to tax thresholds, registration requirements and investment incentives.

Yet the Minister of Finance can only do so much. Remember what an enabling environment entails: quality infrastructure, a deep, skilled labour market, and a predictable regulatory environment. In South Africa today, there are many other barriers that prevent firms from thriving: labour regulations that make it difficult to appoint workers, licensing backlogs, port delays, crime, and endless red tape for the most basic things. A business that saves two hours a week on VAT compliance but loses two days waiting for a municipal permit is no better off.

Operation Vulindlela, the joint initiative between the Presidency and National Treasury, is one attempt at tackling the most pressing bottlenecks – in energy, water, telecommunications and transport. But if the Government of National Unity really wants to make an impact, every Minister in government would ask themselves: what have I done today to make it easier for firms to grow?

The 2026 Budget is a good place to start.

Verhoogen, Eric. “Firm-level upgrading in developing countries.” Journal of Economic Literature 61, no. 4 (2023): 1410-1464.

Visagie, Justin, Ivan Turok, and Andrew Nell. “Creative Destruction or Just a Reshuffle? Turnover Among Businesses and Jobs in South Africa.” South African Journal of Economics 94, no. 1 (2026): e70010.

Kreuser, Carl Friedrich, and Carol Newman. “Total factor productivity in South African manufacturing firms.” South African Journal of Economics 86 (2018): 40-78.