The economic stories we tell

Story-telling is as old as civilization. Around the fire, in religious texts, and in children’s books, stories give us identity, teach us right from wrong, and inculcate us with the norms and values that help us make sense of the world around us.

Economists are beginning to understand that stories also shape our behaviour, and therefore our economic outcomes. In a new NBER paper, financial economist Robert Shiller, the 2013 Nobel-prize winner, calls for the study of what he calls ‘economic narratives’. He argues that the way we talk about certain events, the stories that were told during the Great Depression (of the 1930s) or the Great Recession (of 2007) or even the stories we tell of Trump’s economic policies today, affected (or will affect) the outcomes of these events. Business cycles, he explains, cannot only be explained by the rationality of numbers. The stories we tell, and how these stories spread, matter too.

Economic stories or narratives are simplified ways to help us understand the world. They can take many forms: from newspaper articles and books, to memes, anecdotes, and even jokes. They often appeal to us not because they account for all facts, but because they explain the world in a way that strengthens our existing biases and beliefs. And their success is unpredictable: consider how difficult it is to identify the next ‘hit’ on YouTube or cultural trend to go ‘viral’.

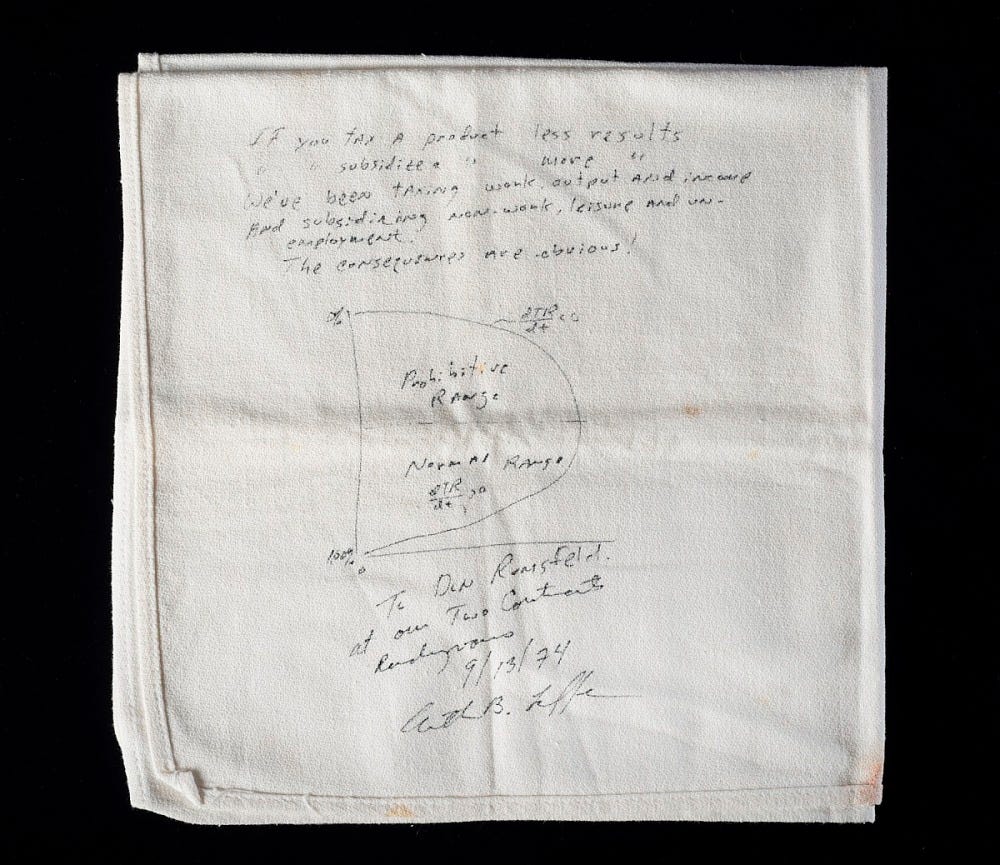

Shiller uses, well, a story to explain the impact of stories. One evening in 1974, at the Two Continents in Washington DC, economist Arthur Laffer had dinner with White House influentials Dick Cheney and Donald Rumsfield. They discussed tax policy, and Laffer took a napkin and drew an inverted-u graph. On the left side, tax rates were 0%, which means tax income was also zero. On the right side, tax rates were 100%, which meant that no-one would work and tax income would also be zero. The point of the curve was to show that there is an optimal tax rate where tax income cannot increase further, whether you increase or decrease tax rates.

This meeting in 1974 would not have been remembered, was it not for the story-telling powers of Jude Wanniski, who wrote a colourful article in National Affairs about the dinner four years later. The story went viral (see image), and had a massive impact on Ronald Reagan’s election as US president in 1980 and his commitment to cutting taxes. (He argued that cutting taxes could increase tax revenue because America was on the wrong side of the Laffer curve). This story was so powerful that a napkin with a Laffer curve is today displayed in the National Museum of American History.

Shiller is, of course, not the first to argue that stories matter. A few years ago, Barry Eichengreen, professor of Economics at UC Berkeley, explained in his presidential speech to the Economic History Association that, while scientists use deductive or inductive reasoning in their research, policy-makers often rely on analogical reasoning. He knows this from experience: when the severity of the Great Recession became known in 2007, policy-makers realised they had to act fast. Had they followed a deductive approach, they would have had to agree on the theoretical reasons for the crisis. Eichengreen argues that this was almost impossible given the deep divides in the field of macroeconomics. Had they followed an inductive approach, they would have had to rely on statistical evidence, much of which was not available immediately.

So instead they turned to an event that they had studied: the Great Depression of the 1930s. Ben Bernanke, who was a student of the Great Depression, used analogical reasoning to ensure that the same mistakes were not repeated. Expansionary monetary and fiscal policy followed. The analogy with the Great Depression also made it easier to communicate their policy response to the broader public. Instead of trying to explain theory or statistics, they could construct a narrative that helped people understand why quantitative easing or fiscal stimulus was necessary. If stories matter in shaping our response to economic events or in persuading us of the validity of some economic policies, what should economists do about it? Shiller suggests that we should incorporate textual analysis into our research: “There should be more serious efforts at collecting further time series data on narratives, going beyond the passive collection of others’ words, towards experiments that reveal meaning and psychological significance.” But this is difficult: “The meanings of words depend on context and change through time. The real meaning of a story, which accounts for its virality, may also change through time and is hard to track in the long run.” New techniques in data science may help.

Eichengreen proposes more emphasis on the study of history. Consider the case of a bank failure in South Africa today. What will we use as policy response: theory, statistics, or earlier bank failures, like Saambou and African Bank? Probably the latter. The problem, Eichengreen warns, is that there is not a single version of history. We all have our ideological glasses through which we look at the past. This is especially true when the facts of what had happened during these past failures are not widely known. The recent Bankorp saga comes to mind.

Because ‘historical narratives are contested’, Eichengreen suggests, we should see ‘more explicit attention to the question of how such narratives are formed’. In other words, if we want to improve our understanding of the world and our ability to predict the future, it’s time economists learn how people tell stories, and how these stories persuade us to behave differently.

*An edited version of this first appeared in Finweek magazine of 23 February. Image source: National Museum of American History.