The battle between passive and active investing

The Index Card is a popular personal finance book, first published in 2017. Its thesis is simple: buy an index fund – like the ALSI top 40 – rather than pay the fees of asset managers, who in the long-run rarely outperform the market. I asked Nico Katzke, Head of Portfolio Solutions at Satrix, why we should not all follow the Index Card’s advice and go for passive rather than active investing.

‘The debate has often been framed, wrongly in my opinion, as either active or passive. In reality, both have their place. Active managers have an important price discovery role to play and preserve the ability to outperform indexes. Index tracking funds, often referred to as passive funds, provide investors with a low-cost alternative, while tracking indices that have proven to be very hard to outperform consistently.’

But even passive investing is not that simple. ‘In reference to Index funds, passive is a bit of a misnomer. Our research shows that the tracking error between two widely tracked indices, the Capped SWIX and the ALSI Top 40, is in line with that of the median active manager to the Capped SWIX. This suggests that your choice of index to track is a very active decision, and not all indices are created equally.’

The main advantage of indices, though, is the fee structure. The ‘Tyranny of fees’, as the The Index Card makes clear, can be devastating for future returns. Is that true in the South African context too?

‘Increasingly, the argument for index tracking investing can be made from both a performance, as well as cost perspective. The two cannot easily be separated though, considering the erosive impact of fees. Indeed, the surprisingly large impact that compounded fees have on investment returns can be summarised in Figure 1. It shows that if you invested R1m at the inception of SA’s first index tracker, the Top 40 Index, what your return profile would’ve been had you been paying different fees. Because it is incredibly hard for active managers to consistently outperform low-cost indexes sufficiently to mitigate the impact of their fees, it is therefore no surprize that such a large cohort fails to outperform index trackers.’

It is time to have active asset managers defend their craft. I asked Paul Theron, founder and CEO of Vestact, a Johannesburg asset management firm, whether active management still has value:

‘Most people are better off buying and holding an index fund like the S&P500 than investing by themselves. Owning an index tracker is definitely better than trying to day trade penny stocks or time the market.’

‘Our fee is 1% per annum, and we’ve beaten the S&P500 handily over 15, 10 and 5 years by being more focused on some sectors (like tech) and less on others (like basic materials, oil and gas). Our services also appeal to those who enjoy owning actual shares. Some of our success is due to stock picking, but it could be that encouraging clients to hold onto their shares in tough times is just as important.’

Mia Kruger, Director at Kruger International, stress the diversification that comes with active management. At Kruger International, we combine indexing strategies with investments into assets like renewable energy and infrastructure projects. Renewable energy and infrastructure projects have not been available to retail investors in South Africa up until last year when we brought the first investment into a windfarm to our clients. Buying an ETF will rarely fulfil all your investment needs. Besides, it is not that easy to pick the right ETF as there are so many and they don’t all charge the same low fees.’

From the two responses, two things stand out: the need to manage investors’ own ‘animal spirits’ and the need for diversification. Let’s tackle the first. Retail investing is becoming increasingly popular, as the valuation of Robinhood Markets, an American online trading platform, suggests. Is it not likely that investors will simply manage their own active portfolios, and leave the rest to index funds?

‘New generation investors are more astute,’ says Katzke, ‘asking difficult questions around value added by active managers in relation to fees. Index providers are also coming to the party by providing new generation investors with the tools to manage their own investments. Platforms like EasyEquities make investing in single stock names easy to do, while SatrixNOW similarly makes investing in a wide range of well-diversified index tracking funds simple.’

But both Kruger and Theron warn against retail trading. Says Kruger: ‘There is a big difference between speculating and investing. The majority of Robinhood’s clients are traders not investors. Most asset managers already manage money for retail investors.’ And Theron: ‘Most retail investors on platforms like Robinhood lose money. So no, I don’t think that they pose a threat to asset managers that are cautious, well-organised and offer a good service. Most clients like to have a sensible advisor to talk to.’

On to diversification. The JSE has seen tepid returns over the last five years. The opportunity set is shrinking as more companies delist. Would you recommend any alternative asset classes?

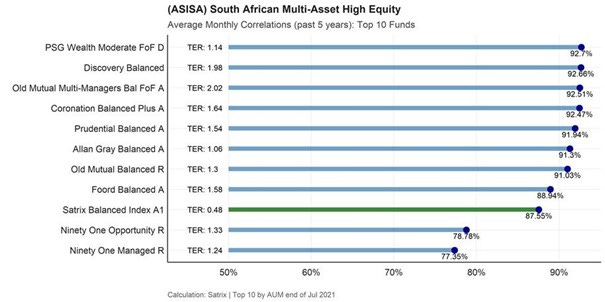

‘Diversification should be framed more accurately in public discourse,’ explains Katzke. ‘True diversification is not about “N” diversification, but rather about risk-source diversification. A portfolio of 100 very similar assets can be less diversified than holding two distinct assets. I strongly feel that true diversification requires placing your eggs in uncorrelated baskets, not merely different ones. The focus is frequently on diversification within asset classes (say, equities) and less on diversification between asset classes. Figure 2 shows the monthly correlations vs TER of the top 10 managed funds, including the Satrix balanced fun. The correlation is incredibly high. I’m not sure most investors know that they are paying active management fees for something that is so highly correlated.’

Theron agrees with the need for diversification, but diversification within a global opportunity set. ‘I’d argue that holding a funny little regional index like the ALSI Top 40 is not a well-diversified investment in global terms.’ Kruger adds that there are other asset classes that are not available to the regular investor. ‘In October 2020 the Kruger Funds became the first unit trusts in South Africa to invest in a wind farm – the Tsitsikamma Community Wind farm through the Gaia Fund 1 company that we listed on the 4 Africa Exchange. We are currently busy with more investments in the alternative asset class of renewable energy and infrastructure. We think that this area offers very attractive investment opportunities, especially in a country like South Africa. So effectively we believe true active management refers to bringing these investment opportunities to retail investors.’

For both active and passive asset managers, guiding investor behaviour and diversifying their offering will be key. New technologies that give investors more information will bring more competition and more choice, pushing down prices. That can only be a good thing for investors worried about their future earnings.

Photo by Aleks Marinkovic on Unsplash.