Neoliberal what what

Ideology and South African economic policy

Lihle, a young economics graduate, had just been offered a job at South Africa’s Parliamentary Budget Office. Before starting, she wanted to understand the past three decades of the country’s economic performance. Her professors had talked about ‘low growth’, ‘deindustrialisation’, and ‘fiscal constraints’, but they’d offered few clear answers. She began reading more widely, hoping for perspective. Instead, she found confusion.

Two recent pieces – one by Seeraj Mohamed in New Agenda and another by Eustace Davie for the Free Market Foundation – offered sharply opposed diagnoses. Neither was neutral, nor necessarily representative of the academic consensus. But they each illustrated a dominant pole in South Africa’s public debate.

Mohamed’s article blames South Africa’s deepening economic malaise on the adoption of neoliberal economic policies after 1994. He claims these policies, imposed with the help of corporate elites, enabled rent-seeking, financialisation and speculative behaviour rather than productive investment. The country was ‘denuded, deindustrialised and financialised’, he writes, while government continues to impose suffering on the majority through its adherence to austerity and market-friendly reforms. The solution, Mohamed argues, is to return to a state-led developmental model with more central planning, capital controls, and state-directed investment.

Davie, writing for the Free Market Foundation, offers a diametrically opposite view. He denies that South Africa has ever truly embraced neoliberalism. Far from liberalising, Davie argues, the post-apartheid state entrenched regulatory complexity, rigid labour laws, and state dominance through extensive social spending and over-regulated markets. He sees South Africa’s decline not as the product of free markets, but of government failure, rent extraction and policy uncertainty. Redistribution without growth, he argues, is a mirage. The only way forward is through liberalisation, institutional reform and the expansion of economic freedom.

Two articles and two narratives. One faults government, the other the market.

But does either side really explain what happened?

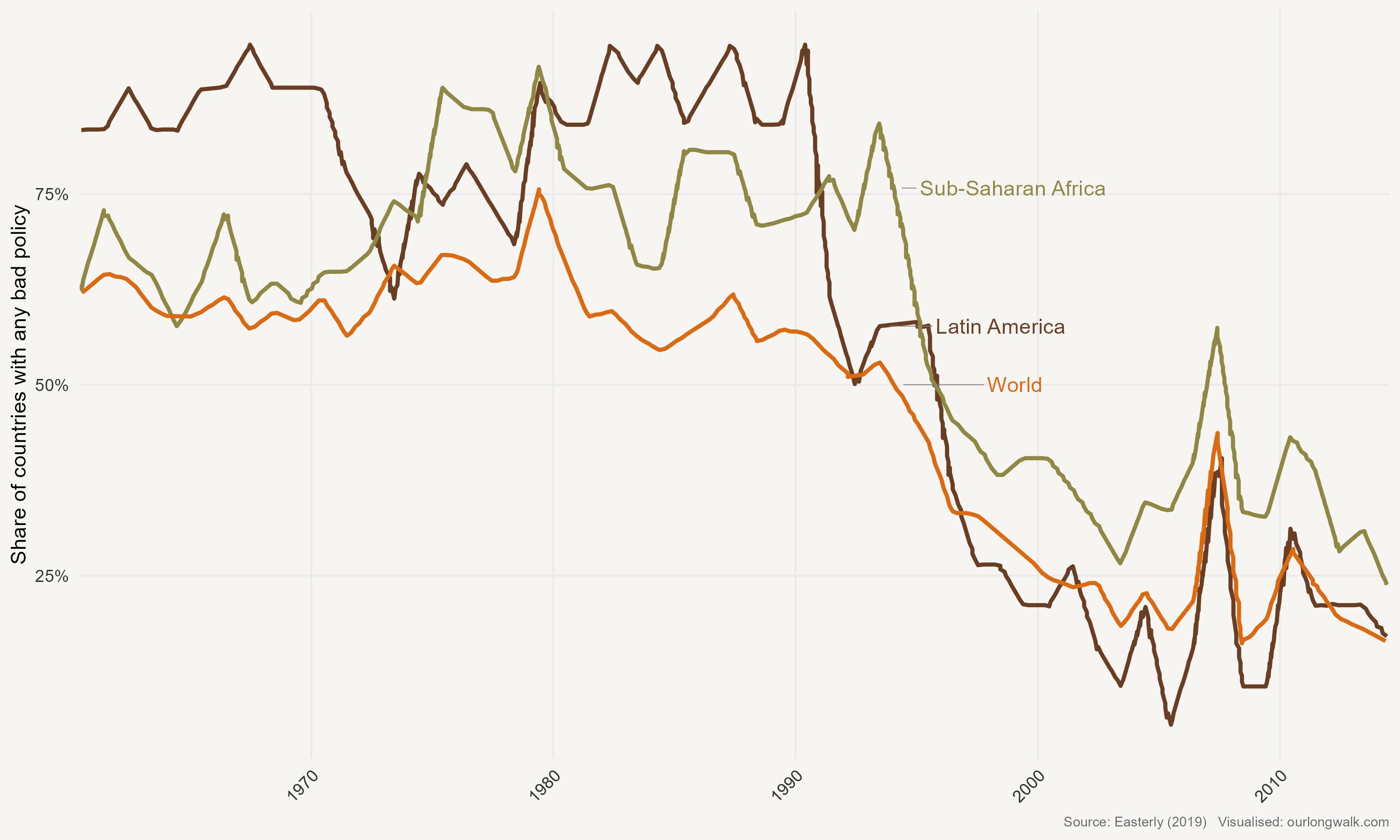

To find it, we must step back – beyond South Africa, beyond the 1990s – and look at the broader arc of African economic history. The term ‘Washington Consensus’ is often used, usually pejoratively, to describe the liberalising economic reforms promoted by the IMF and World Bank in the 1980s and 1990s: cutting deficits, stabilising currencies, removing trade barriers, liberalising prices. The outcomes of these reforms seemed dismal at first. Economic growth in Africa stagnated or declined. Famine in Ethiopia, genocide in Rwanda, and deepening poverty elsewhere seemed to confirm that the ‘structural adjustment’ era had failed. Critics, including respected economists like William Easterly, were quick to denounce the Washington Consensus as another failed foreign prescription.

But that early judgement, as it turned out, was premature. In a 2019 working paper, Easterly revisited his own earlier views. He found that many of the reforms once maligned for their lack of immediate results had longer-term payoffs. Drawing on updated data, he showed how the number of countries with so-called ‘bad policies’ – runaway inflation, currency black markets, excessive price controls – fell dramatically in the late 1990s and early 2000s. The figure accompanying his paper shows this sharp decline. And as these distortions disappeared, economic growth in Africa and Latin America returned.

A 2021 paper by Belinda Archibong, Brahima Coulibaly and Ngozi Okonjo-Iweala confirms the trend. In the 1980s and 1990s, economic growth in Africa averaged less than 0.2 percent per year. But from 2000 to 2019, that figure rose to 1.6 percent – eight times higher. Inflation fell dramatically. Fiscal deficits narrowed. Investment returned to key sectors like telecoms, retail, and manufacturing. ‘These changes’, they write, ‘did help to attract more private investment in key sectors… that accounted for a significant share of the growth increases in the 2000–2019 period’. Reforms worked: not immediately, not perfectly, and not everywhere, but they laid the foundation for growth.

South Africa’s own story fits this pattern. After 1994, the ANC adopted the Reconstruction and Development Programme (RDP), a social spending-focused plan. But facing fiscal constraints and sceptical investors, the government pivoted in 1996 to GEAR – the Growth, Employment and Redistribution strategy. GEAR committed to fiscal consolidation, inflation targeting and investment-friendly reforms. Critics derided it as neoliberal austerity. And indeed, the short-term results were not spectacular: unemployment remained high, and growth averaged a modest 2.5 percent.

But from the early 2000s, things changed. Growth accelerated, averaging over 5 percent between 2004 and 2007. Inflation stabilised. Debt fell. Government revenue outpaced spending. This afforded the government the chance to shift more resources through the budget to those who needed it most, ensuring that poverty declined, especially when measured using multidimensional metrics. By 2008, South Africa had recorded its strongest economic performance and largest reduction in poverty, supported by macroeconomic stability, commodity prices and the tailwinds of global demand.

The next decade tells a cautionary tale. After President Zuma took office in 2009, the rhetoric shifted towards state-led development. The budget ballooned. Government wages grew well above inflation. State-owned enterprises expanded in size but not in effectiveness. Eskom, Transnet and others became vehicles for patronage and corruption. Electricity outages returned. Public trust eroded. Investment dried up. Growth collapsed. Between 2010 and 2024, per capita GDP remained exactly the same. The policies had changed, but the results were worse. Mohamed’s article, curiously, makes little mention of this.

The lesson from both Africa and South Africa is not that neoliberalism saves, or that state-led development destroys. It is that good policies demand sound empirical evidence. Some of the most successful periods of growth occurred when governments implemented targeted, market-oriented reforms backed by macroeconomic discipline, credible institutions and policy coherence. And some of the most damaging setbacks occurred when governments lost fiscal control, weakened the rule of law, or pursued ideology over evidence.

To call every liberalising reform ‘neoliberalism’ or every fiscal discipline measure a ‘Washington Consensus relic’ is to reduce economic policy to caricature. These terms have become so vague, so ideologically loaded, that they hinder rather than help debate.

This is not a uniquely South African problem. In the United States, writers like Matt Yglesias and Noah Smith have both criticised the way ‘neoliberalism’ has become a catch-all insult, emptied of analytical precision. Yglesias, in a series on Neoliberalism and Its Enemies, notes that many supposed ‘neoliberal’ outcomes – like the expansion of welfare programmes or the persistence of regulation – do not fit the caricature. Smith similarly argues that the real influence of neoliberalism was not a radical policy turn, but a shift in framing: a set of assumptions about what government could or could not do. That shift made it harder, for example, to propose industrial policy or climate interventions.

Such labels can carry a heavy cost. As Matías Kulfas explains in the context of Argentina, the real danger is when economic tools are ruled out because of their ideological association. Fiscal or monetary expansion can be effective, but only if well-timed. Capital inflows can support growth, but only if prudently managed. ‘To govern is to explain’, Brazil’s former president Fernando Henrique Cardoso once said. Pretending that there are no trade-offs – that ideology can substitute for analysis – only undermines trust.

South Africa needs less rhetoric and more realism. We need more data and fewer slogans. A school voucher scheme may work. So might labour reform. Or capital controls. Or public employment programmes. Or any mix of these. But their success depends on execution, sequencing and institutional capacity, not on whether they come with the correct ideological label.

A week into her new job, Lihle sat in a meeting where a colleague dismissed a proposed economic reform as ‘too neoliberal’. No further explanation. No data. No discussion. Just a label, used to shut down the idea. She looked around the room and wondered: if our policymakers are unwilling to test new ideas, to learn from the past, and to adapt to new realities, who will write the policies that can get South Africa growing again?

For those wondering, ‘what what’ is a colloquial South African expression often used for humour or ambiguity, especially when the speaker is being dismissive or ironic. It can imply ‘and all that stuff’ or ‘whatever that means’. An edited version of this article was published on News24. Support more such writing by signing up for a paid subscription. The image was created with Midjourney v6.

That title is just 👌🏾👌🏾.. I remember someone telling me- you economics people are so obsessed with numbers!

And I was like, of course we are… if you are going to make decisions that affect lots of people you better have data and deep analysis that backs the decision-making.. Lived experience is too narrow and also biased to be a guiding post for decisions that affect millions

Beyond the ideological tagging, i think people think that when we analyze these numbers, it’s all made up and they don’t mean much…there is idea that when we talk people it has to be story driven only and not numbers driven… av heard people talk about “GDP are just made up numbers that don’t really reflect living conditions”…

So I think the tying the stories to the numbers is super important..which is what you are doing..

Loved the post! 😊

Well written, reseached and argued, Johan.