Bigness is goodness

Large firms, not small ones, will solve South Africa's jobs crisis

A good friend recently began to work for a large firm in South Africa. He tells me that he’s been surprised at the productivity of the team; having just returned from a venture firm in Europe, where he thought they were working hard to keep the dream of future gazillions alive, he expected a slightly more relaxed lifestyle here. But it is just the opposite. Their main markets are outside of South Africa, so they have to compete not only against the best in South Africa, but the best globally. Success, here, doesn’t just mean higher (future) returns for the owners. It means higher salaries, more jobs – for both skilled and semi-skilled workers – more taxes for government. In short: it means economic growth.

His story got me thinking. South Africa has a Department of Small Business Development. It has programmes, grants, and incubators dedicated to helping entrepreneurs start small. It does not have a Department of Large Firm Competitiveness. Perhaps it should.

That is because the uncomfortable truth is that small firms – however admirable their hustle – are not the ones that will move the needle. Large firms will.

That claim sounds unfashionable, even harsh. So let me show you the evidence.

A striking new paper by Zhang Chen, forthcoming in Econometrica – one of the most prestigious journals in economics – documents a simple but powerful fact: as countries grow richer, the right tail of the firm size distribution thickens. In plain language: economic development means more large firms, and larger large firms. This is not a comparison of apples and oranges – rich countries versus poor countries at a single point in time. It holds within countries over time. As an economy grows, its biggest firms grow even bigger relative to the rest. Chen shows this for a panel of 33 OECD countries from 2008 to 2017 and for the United States over four decades. The relationship is robust across sectors and across different ways of measuring firm size.

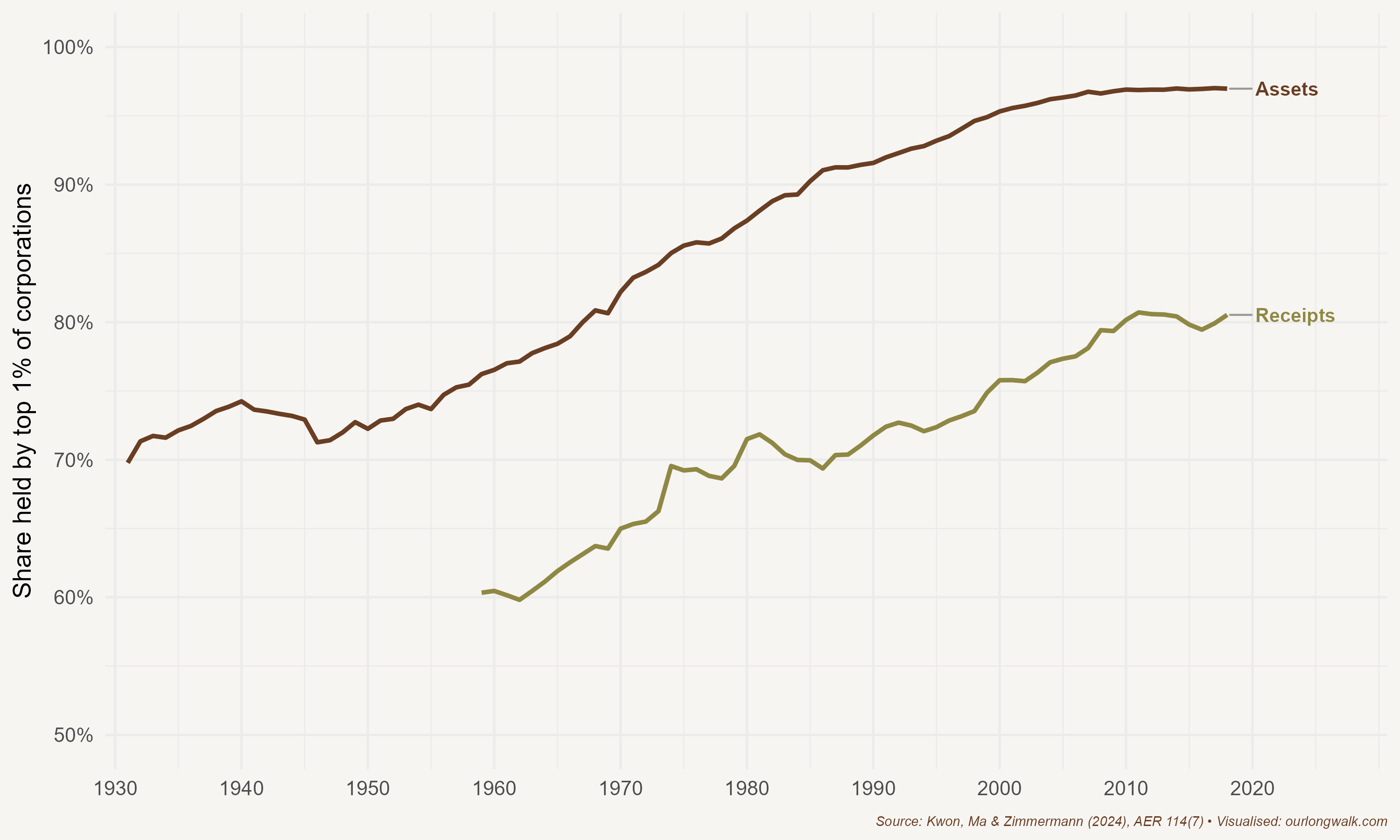

The pattern is remarkably persistent. Spencer Kwon, Yueran Ma, and Kaspar Zimmermann collected data on the size distribution of US businesses stretching back a full century. Their finding, published in the American Economic Review in 2024, shows that in the early 1930s, the top 1 per cent of US corporations held about 70 per cent of total corporate assets. By 2018, that figure had risen to 97 per cent. The top 1 per cent’s share of receipts – a proxy for sales – climbed from around 60 per cent to over 80 per cent. This is not a recent Silicon Valley story. It is a hundred-year secular trend. Each generation, it turns out, believes itself to be witnessing something new. Each generation is wrong. Bigness has been rising for as long as we have measured it.

But why? Is it just that rich countries happen to have big firms, or is there a deeper mechanism at work?

Chen’s theoretical contribution offers a compelling answer. He builds a model of what he calls ‘idea search’: firms improve their productivity by learning from other, more productive firms. Think of it as economic osmosis. A mid-sized manufacturer does not figure out a better logistics system from scratch. It learns by hiring someone who worked at a bigger firm, by observing what a competitor does, or by absorbing knowledge through a supply-chain relationship. When firms search for better ideas – new technologies, new processes, new ways of organising production – they are more likely to learn from the most productive firms in the economy. And those are, almost by definition, the large ones.

This creates what economists call a ‘diffusion externality’. When a large firm innovates or adopts a better process, the benefits do not stop at its factory gates. Its suppliers learn. Its competitors are forced to adapt. Its former employees carry knowledge into new ventures. The entire economy benefits. Put differently, when a large firm in Johannesburg figures out how to do something better, that knowledge ripples through its suppliers, its competitors, and eventually the entire economy.

The problem is that large firms do not capture the full social value of this diffusion. They invest in idea search for their own benefit, not for the benefit of the firms that learn from them. The result: they under-invest relative to what would be socially optimal. Chen shows that policies favouring large firms can correct this market failure and improve welfare. This is not a defence of cronyism or monopoly. It is a precise economic argument about externalities – the same logic that justifies subsidising education or vaccinations.

What does this mean for South Africa?

Start with exports. Marianne Matthee and her co-authors showed, in a 2017 study published in the South African Journal of Economics, that only large, productive firms manage to export manufactured goods from South Africa. Small firms lack the scale, the knowledge, and the networks to compete in international markets. If we want South Africa to earn foreign exchange, we need firms big enough to break into those markets.

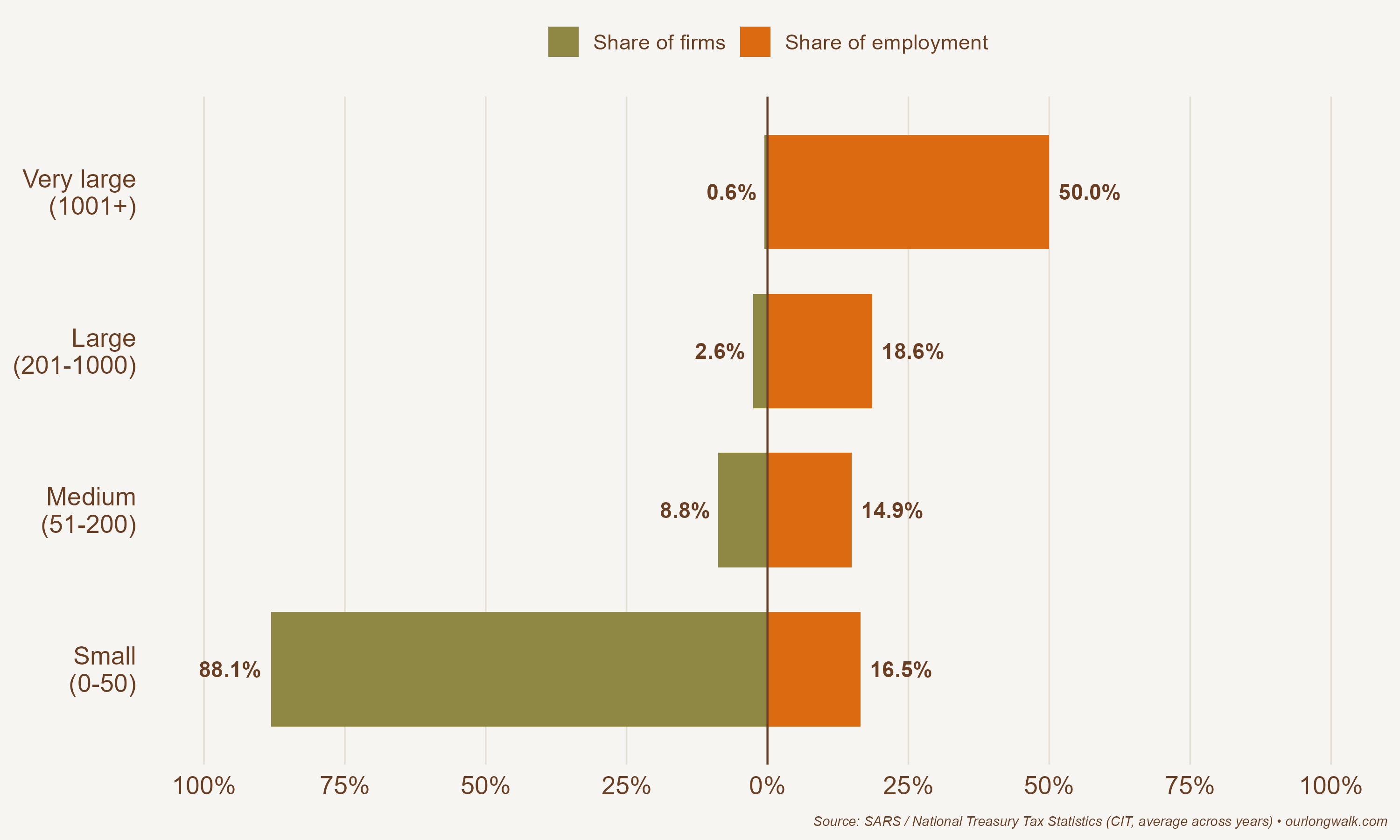

And here is the rub. South Africa already has firms like that – just not nearly enough of them. SARS tax data show that barely a thousand firms employ 1 000 or more workers. They make up roughly half a per cent of all formal firms, yet they account for fully half of all formal employment.

The trouble is what those giants do. South Africa’s large firms tend to come in two flavours: resource extractors that ship commodities, and domestically oriented champions in retail, banking, and telecoms that sell mostly to South Africans. The category we are missing – the large, export-oriented, internationally competitive manufacturer of the kind my friend now works for – is precisely the one Chen’s model tells us matters most for growth.

Then consider market structure. Friedrich Kreuser, Michael Kilumelume, and Rulof Burger, in a 2024 UNU-WIDER working paper, studied markups and mergers in the South African economy. They found that large mergers affect market dynamics through supply-chain integration – a channel that is often overlooked in the competition debate. The policy question is not whether large firms should exist. It is whether they face enough international competition to keep them sharp. A large firm shielded by tariffs and red tape is a drag on the economy. A large firm forced to compete globally is an engine of growth.

To put it into perspective: a single globally competitive firm like Shoprite employs over 150,000 people across Africa. It trains workers, builds cold-chain infrastructure, and anchors local economies in towns where it is often the largest private employer. Discovery, Naspers, Bidvest – these firms sit at the centre of vast supply chains, generating demand for thousands of smaller suppliers. They pay the bulk of corporate tax. They invest in the technologies that other firms eventually adopt. A thousand survivalist spaza shops, however important for the livelihoods of their owners, do not create the same kind of systemic growth. They are a symptom of an economy with too few good jobs, not a cure.

Of course, this does not mean small firms are worthless. They provide livelihoods. They are seedbeds for entrepreneurship. A handful will hopefully grow into the large firms of the future – and a healthy economy needs that pipeline. But the policy emphasis is backwards. Small firms benefit most when large firms thrive – as suppliers in their value chains, as employers of skilled workers who later start their own businesses, as anchors of local economies that generate demand for everything from catering to courier services. Chen’s model makes this precise: the diffusion externality flows from large firms to the rest of the economy, not the other way around.

The problem is not that South Africa has too few small firms. It is that too few of its large firms compete globally. And when those firms are hemmed in by red tape, unreliable electricity, crumbling rail networks, and policy uncertainty, the damage is not limited to their balance sheets. It cascades through the entire economy.

Which brings us back to my friend. His large firm’s intensity is not an accident. It is the price of global competition. And it is precisely that competition – gruelling, relentless, sometimes exhausting – that makes the firm a growth engine for the rest of the economy. Every rand it earns abroad, every idea it absorbs and diffuses, every worker it trains lifts the broader economy in ways that no government programme for small business can replicate.

The lesson? If South Africa wants jobs, stop romanticising smallness. Make sure the big firms can compete with the best in the world. Their success will not just enrich their shareholders. It will ripple through the entire economy – into the salaries of their workers, the orders of their suppliers, and the tax receipts that fund schools and clinics. Bigness, it turns out, is goodness.

Great piece! I love the perspective here. I’d just add that since all big companies were small once, a thriving economy really needs that 'pipeline' of small businesses growing into big ones. Supporting the little guys isn't necessarily a bad move by the government, even if it’s hard to get the policy exactly right. Thanks for sharing this!

A small anecdotal complement: working in debt financing, I learned that small business lending rest in large part on the quality of the collateral and, even more important, the chances to sell it in case of bankruptcy. Those features depend on the existence of a sufficiently deep market of those assets and the financial back of the players of those markets. Then, the existence of large players appreciates the worth of the collateral, allowing smaller firms to borrow, and, paradoxically, fueling competition